Currently Empty: $0.00

17.2 Initiating a Mortgage Loan

17.2 Initiating a Mortgage Loan

The mortgage loan process begins when the borrower completes a loan application and submits it to a lender. In this topic, you’ll learn what’s included in the application package and what underwriting is designed to evaluate.

The Loan Application

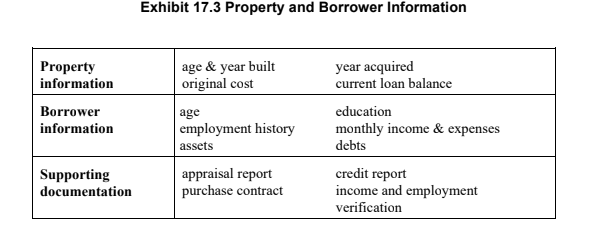

Most lenders use a version of the Uniform Residential Loan Application (commonly associated with Fannie Mae). The application collects information about the property and the borrower, and it must include supporting documentation.

Completion matters: The application must be complete, signed, and dated before the lender will evaluate it.

The application typically includes the requested loan amount based on the underlying transaction (purchase, refinance, etc.). The process is considered “initiated” when the lender receives the completed application package.

Important note: Federal law requires lenders to accept applications and provide notice about the disposition of the application.

Mortgage Loan Underwriting

Underwriting is the process of assessing the lender’s risk in making the loan. Underwriters evaluate both the borrower and the property.

What the lender is trying to determine

- Borrower risk: ability and willingness to repay (income, cash reserves, credit, employment stability).

- Property risk: whether the collateral value is strong enough to cover potential losses.

- Loan terms: the interest rate, term, and structure that fit the risk profile.

Loan-to-Value Ratio (LTV)

The loan-to-value ratio (LTV) is the relationship of the loan amount to the property value, expressed as a percentage. Lenders typically lend only a portion of the property’s value. The difference is covered by the borrower’s down payment.

Example: If the lender’s LTV limit is 80%, the maximum loan on a $100,000 property is $80,000 (the borrower must cover the remaining $20,000).

Private Mortgage Insurance (PMI)

If the LTV is high (meaning the borrower has little equity), the lender may require private mortgage insurance (PMI). PMI protects the lender for the portion of the loan above a typical LTV threshold (often 80%).

PMI in plain English: It’s an extra layer of protection for the lender when the borrower’s down payment is small.

Quick Check-Ins (Self-Test)

1) Mortgage loan underwriting is primarily the process of:

- A. Recording the deed at the courthouse

- B. Assessing the lender’s risk by evaluating the borrower and the property

- C. Setting the home’s listing price

- D. Choosing a title company

Show Answer

Correct: B. Underwriting evaluates borrower ability to repay and the property’s value as collateral.

2) A lender requires PMI most commonly when:

- A. The borrower has a low loan-to-value (LTV) ratio

- B. The borrower’s down payment is large

- C. The loan-to-value (LTV) ratio is high

- D. The borrower pays points at closing

Show Answer

Correct: C. PMI is commonly required when LTV is high (small down payment, less equity).