Currently Empty: $0.00

17.3 Qualifying for a Mortgage Loan

17.3 Qualifying for a Mortgage Loan

To qualify for a mortgage loan, borrowers must meet lender standards for income, debt, cash reserves, net worth, and credit. This topic covers ECOA protections, the key qualification ratios, and the loan constant concept used to estimate payments and borrowing power.

Equal Credit Opportunity Act (ECOA)

The Equal Credit Opportunity Act (ECOA) requires lenders to evaluate applicants based on their own income and credit, unless the applicant asks to include another person’s information. ECOA also prohibits discrimination in lending decisions.

Key protection: If a lender denies a loan or offers different terms, the lender must provide written notice with specific reasons.

Qualifying the Borrower (Ability to Repay)

Lenders assess whether the borrower can reasonably repay the loan. Underwriting commonly considers income/assets, employment status, credit history, the proposed mortgage payment, other debts, and the borrower’s debt-to-income ratio (DTI).

Important: For adjustable-rate mortgages (ARMs), qualification generally uses the highest rate the borrower might have to pay (not a temporary “teaser” rate).

Income Ratio and Debt Ratio

Many lenders use two key ratios to estimate affordability:

Income Ratio (Housing Ratio)

Limits the percent of gross monthly income that can be spent on housing costs (often PITI and related housing expenses).

Debt Ratio (Housing + Debt)

Considers housing costs plus other monthly debt obligations (credit cards, car loans, etc.).

Reminder: Ratio standards vary by lender and loan type (conventional vs. FHA vs. VA), and they can change over time.

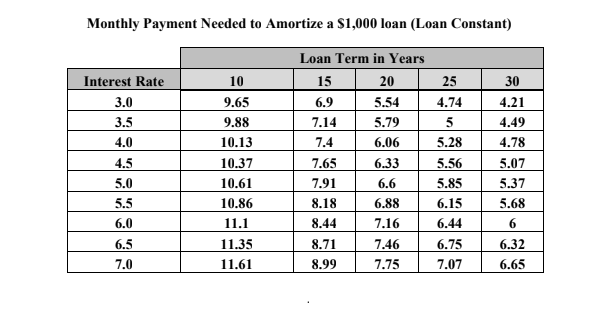

Loan Constant (Payment Shortcut)

A loan constant is a pre-calculated number that relates the monthly principal-and-interest payment to a $1,000 loan amount for a specific interest rate and term. It helps estimate:

- the monthly PI payment for a given loan amount, rate, and term

- the loan amount a borrower can afford based on a monthly PI budget

How it’s used:

(Loan amount ÷ 1,000) × Constant = Monthly PI payment

(Loan amount ÷ 1,000) × Constant = Monthly PI payment

And the reverse:

(Monthly PI payment ÷ Constant) × 1,000 = Loan amount

(Monthly PI payment ÷ Constant) × 1,000 = Loan amount

Other Qualification Factors

- Cash qualification: lender verifies funds for the down payment (gift letters may be required for gifts).

- Net worth: shows reserves and ability to sustain payments during disruptions (like job loss).

- Credit evaluation: lender reviews credit report/score and public record items (judgments, bankruptcies, foreclosures, etc.).

- Loan commitment: written pledge to lend under specific terms (firm, lock-in, conditional, take-out).

Key term: A lock-in commitment protects the borrower from rate increases for a set period (often for a fee/points).

Quick Check-Ins (Self-Test)

1) The loan constant is used to:

- A. Determine the legal description of a property

- B. Estimate monthly PI payments or affordable loan amount based on rate/term

- C. Replace the need for underwriting

- D. Set the down payment requirement by law

Show Answer

Correct: B. Loan constants help estimate payments or loan amount for a given interest rate and term.

2) ECOA is primarily designed to:

- A. Standardize closing costs nationwide

- B. Prohibit discrimination in extending credit

- C. Guarantee all VA loans

- D. Set the Federal Reserve discount rate

Show Answer

Correct: B. ECOA prohibits discrimination in lending and requires fair evaluation of applicants.