Currently Empty: $0.00

17.1 Anatomy of Mortgage Lending

17.1 Anatomy of Mortgage Lending

Most real estate purchases involve borrowed money. In this topic, you’ll learn the basic mechanics of mortgage financing, the key financial components of a loan, and the purpose of the promissory note and the mortgage (or deed of trust).

Mechanics of a Loan Transaction (Big Picture)

When a borrower signs a promissory note (promise to repay) and gives the lender a mortgage (or deed of trust) as security, the financing method is called mortgage financing.

The process of securing a loan by pledging property without giving up ownership is called hypothecation.

Two required instruments:

- Note = evidence of the debt

- Mortgage / deed of trust = evidence of the collateral pledge

Lien-Theory vs. Title-Theory (Ownership View)

- Lien-theory states: the mortgage creates a lien against the property; the borrower retains title.

- Title-theory states: the mortgage (or trust deed structure) is treated more like a conveyance of title to secure the loan.

- Intermediate theory: combines aspects of both approaches.

Why it matters: The theory affects how states treat lender/borrower rights, especially during default and foreclosure.

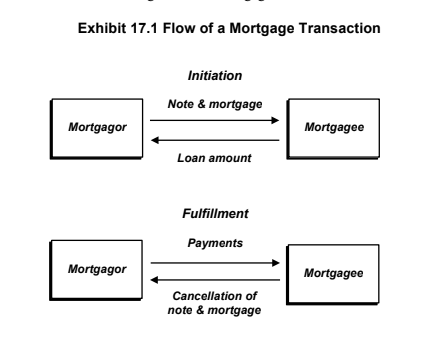

Mortgage Transaction Flow

- Initiation: borrower delivers the note and mortgage; lender delivers the loan funds.

- Fulfillment: borrower makes payments over time.

- Cancellation: once paid off, the note and mortgage are cancelled/released.

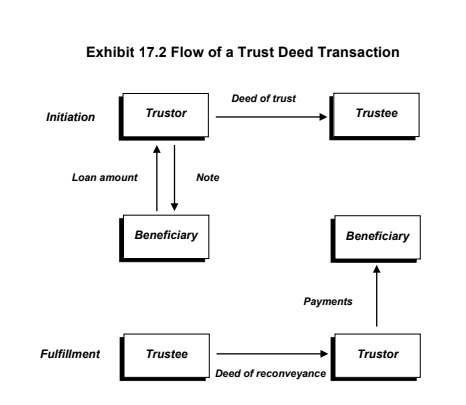

Deed of Trust Transaction Flow

A deed of trust involves a third party trustee. The borrower (trustor) conveys title to the trustee as security for the loan. The lender is the beneficiary.

- Initiation: trustor signs note + deed of trust; lender funds the loan.

- During the loan: trustee holds title on behalf of the beneficiary (lender).

- When paid off: trustee issues a deed of reconveyance back to the borrower.

Financial Components of a Loan

- Principal: the amount borrowed (original principal); remaining unpaid principal is the loan balance.

- Interest: the charge for using the lender’s money; can be fixed or adjustable.

- APR: required disclosure that reflects the interest rate plus certain finance charges.

- Points: prepaid interest (1 point = 1% of the loan amount) used to increase lender yield.

- Term: the length of time until the loan must be paid off (balloons can shorten payoff date).

- Payments: usually monthly; in amortizing loans, each payment includes interest + principal.

Usury: Many states limit excessive interest rates by law.

Promissory Note vs. Mortgage/Trust Deed

Promissory Note

- Evidence of the debt

- Borrower’s promise to repay

- States loan amount, term, repayment method, interest rate

- Negotiable instrument (can be assigned to another party)

Mortgage / Deed of Trust

- Evidence of the collateral pledge

- Identifies the property (legal description + address)

- Includes performance clauses (escrow, insurance, maintenance, due-on-sale, etc.)

- Creates the lender’s security interest in the property

Quick Check-Ins (Self-Test)

1) Hypothecation is best described as:

- A. Giving up ownership of the property to get a loan

- B. Pledging property as security without giving up ownership

- C. Paying points to lower an interest rate

- D. Recording a deed of reconveyance

Show Answer

Correct: B. Hypothecation is pledging property as collateral while keeping ownership.

2) Which instrument is evidence of the debt?

- A. Mortgage document

- B. Deed of reconveyance

- C. Promissory note

- D. Title insurance policy

Show Answer

Correct: C. The promissory note is evidence of the debt and the borrower’s promise to repay.