Currently Empty: $0.00

15.1 The Market System

15.1 The Market System

The market system is driven by supply, demand, and the price mechanism. In this topic, you’ll learn how price reflects value, how costs influence production, and how markets move toward (but rarely sit in) equilibrium.

Supply and Demand

The goal of an economic system is to produce and distribute goods and services to satisfy consumer demand.

Supply is the quantity of a product or service available for sale, lease, or trade at any given time.

Demand is the quantity of a product or service desired for purchase, lease, or trade at any given time.

The interplay of supply and demand is what makes an economy work: consumers demand goods and services; suppliers produce and distribute them for a negotiated price.

Price and Value

The Price Mechanism

A price is the amount of money (or other asset) a buyer agrees to pay and a seller agrees to accept to complete an exchange.

In this context, price means the final trading price—not the asking price or the initial bid.

What Creates Value?

Price is a number that quantifies value. The value of something is based on four key questions:

- Desire: How much do I want it?

- Utility: How useful is it—does it do the job?

- Scarcity: How available is it relative to demand?

- Purchasing power: Am I able to pay for it?

Big idea: When the underlying value factors change, price tends to change too.

Productivity and Costs

To produce a good or service, a supplier incurs costs—the expenses necessary to generate and deliver the item to the market.

Essential production costs include capital, materials and supplies, labor, management, and overhead.

Producers must be efficient and price-competitive. If a competitor can produce a similar product for less, higher-priced items are forced out of the market.

Cost and price: For an efficient producer, cost + profit can establish a minimum price needed to stay in business.

Market Interaction

A market is a place (or arena) where supply and demand encounter one another and the price mechanism defines value.

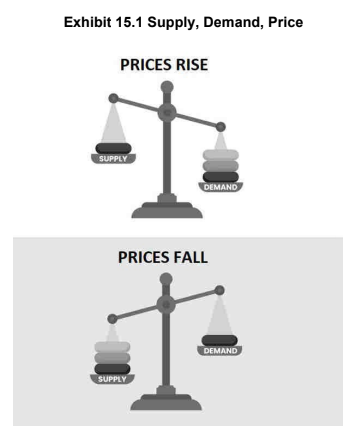

In a market economy, the primary relationships between supply, demand, and price are:

- If supply increases relative to demand, price decreases.

- If supply decreases relative to demand, price increases.

- If demand increases relative to supply, price increases.

- If demand decreases relative to supply, price decreases.

Reverse logic: If price rises, demand is increasing relative to supply. If price falls, demand is declining relative to supply.

Market Equilibrium

Markets tend toward a state of equilibrium where supply equals demand and price, cost, and value are theoretically identical.

In real life, there is usually a time lag between an imbalance and the market’s adjustment—so markets are often in some state of imbalance.

Reality check: Because supply and demand determinants are constantly changing, equilibrium is more of a direction than a permanent condition.

Quick Check-Ins (Self-Test)

1) If demand increases and supply stays the same, what usually happens to price?

- A. Price decreases

- B. Price increases

- C. Price stays the same no matter what

- D. Price becomes equal to the asking price

Show Answer

Correct: B. When demand rises relative to supply, consumers compete and prices tend to increase.

2) Which of the following is NOT one of the four determinants of value?

- A. Desire

- B. Utility

- C. Scarcity

- D. Commission rate

Show Answer

Correct: D. The four determinants are desire, utility, scarcity, and purchasing power.