Currently Empty: $0.00

18.6 Investment Analysis of an Income Property

18.6 Investment Analysis of an Income Property

Income properties are held primarily to generate income (like rent). In this topic, you’ll learn how investors evaluate an income property using cash flow and taxation—starting with pre-tax cash flow, then calculating tax liability, and finally determining after-tax cash flow. You’ll also see common ways investors measure investment performance.

Income Property vs. Non-Income Property

Income properties (including residential rentals and commercial buildings) differ from non-income properties because they can produce an annual income stream—and because deductions for depreciation (cost recovery) are generally allowed on income properties.

Like other real estate, income properties may also create a gain (or loss) on sale.

Key idea: Investors often compare both pre-tax and after-tax results to understand the true productivity of the investment.

Pre-Tax Cash Flow (Cash Flow Before Taxes)

Cash flow is the difference between actual cash coming in (revenue) and cash going out (expenses, reserves, debt service, etc.).

Cash flow includes cash items only, so it excludes depreciation because depreciation is not a cash expense.

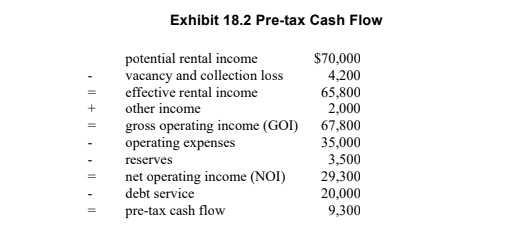

Pre-tax cash flow formula (as presented):

Potential rental income

− Vacancy and collection loss

= Effective rental income

+ Other income

= Gross operating income (GOI)

− Operating expenses

− Reserves

= Net operating income (NOI)

− Debt service

= Pre-tax cash flow

Potential rental income

− Vacancy and collection loss

= Effective rental income

+ Other income

= Gross operating income (GOI)

− Operating expenses

− Reserves

= Net operating income (NOI)

− Debt service

= Pre-tax cash flow

Exhibit 18.2 — Pre-tax Cash Flow

Quick vocabulary: NOI is the income left after operating expenses (and reserves in this presentation), before debt service.

Tax Liability (Based on Taxable Income, Not Cash Flow)

The owner’s tax liability is based on taxable income, which is not the same as cash flow.

Some cash items (like reserves and principal paydown) are not deductible, while some non-cash items (like depreciation) are deductible.

Taxable income formula (as presented):

Net operating income (NOI)

+ Reserves

− Interest expense

− Cost recovery (depreciation) expense

= Taxable income

× Tax rate

= Tax liability

Net operating income (NOI)

+ Reserves

− Interest expense

− Cost recovery (depreciation) expense

= Taxable income

× Tax rate

= Tax liability

In the example from the text, the property’s taxable income is low because depreciation (cost recovery) is a large deduction—even though the property still produces positive cash flow.

Exam-friendly takeaway: A property can have positive cash flow and still show low taxable income because depreciation reduces taxable income.

After-Tax Cash Flow

After-tax cash flow is what the owner actually keeps after paying income tax on the property’s taxable income.

After-tax cash flow formula:

Pre-tax cash flow − Tax liability = After-tax cash flow

Pre-tax cash flow − Tax liability = After-tax cash flow

In the example, the after-tax cash flow is only slightly lower than the pre-tax cash flow because the tax liability is small.

Measuring Investment Performance (Common Metrics)

Investors measure performance in different ways depending on their goals. Common measures include:

- Return on investment (ROI): net operating income divided by price.

- Cash-on-cash return: cash flow divided by cash invested.

- Return on equity: cash flow divided by equity.

- Discounted cash flow analysis and internal rate of return (IRR): more advanced methods that require projected future cash flows and estimated proceeds from sale.

Licensee note: If you don’t have expertise in advanced return calculations (like IRR), refer clients to a qualified investment professional.

Quick Check-Ins (Self-Test)

1) Which item is NOT a cash expense and is therefore excluded from cash flow calculations?

- A. Operating expenses

- B. Debt service

- C. Depreciation (cost recovery)

- D. Reserves

Show Answer

Correct: C. Depreciation is a non-cash deduction, so it does not appear in cash flow.

2) After-tax cash flow is calculated as:

- A. NOI − operating expenses

- B. Pre-tax cash flow − tax liability

- C. Taxable income × tax rate

- D. GOI − vacancy and collection loss

Show Answer

Correct: B. After-tax cash flow equals pre-tax cash flow minus tax liability.