Currently Empty: $0.00

18.5 Investment Analysis of a Residence

18.5 Investment Analysis of a Residence

A primary residence is typically a non-income property, meaning it doesn’t produce rental income (unless a portion is used for business or rent). In this topic, you’ll learn how to evaluate a residence as an investment using appreciation, tax benefits (like mortgage interest), and how gain on sale is calculated for tax purposes.

What “Investment Analysis” Means Here

Investment analysis examines the economic performance of an investment by looking at costs, income (if any), taxation, appreciation, and overall return.

Since a primary residence usually does not generate income, its investment value typically comes from:

appreciation, leverage, and certain tax benefits.

Note: If part of the home is used to produce income (like certain home office situations), that portion may be treated differently for tax purposes.

Appreciation (Increase in Value Over Time)

Appreciation is the increase in value of an asset over time. A simple estimate of total appreciation is:

Total appreciation:

Current value − Original price = Total appreciation

Current value − Original price = Total appreciation

To express appreciation as a percentage of the original price:

Percent appreciation:

Total appreciation ÷ Original price = % appreciation

Total appreciation ÷ Original price = % appreciation

To estimate annual appreciation (simple average), divide the percent appreciated by the number of years owned.

Deductibles (Common Tax Benefit for a Residence)

The primary tax benefit for many homeowners is the annual deduction for mortgage interest (subject to current IRS rules and limitations).

The portion of the mortgage payment that goes to principal is not deductible.

Also, depreciation is not allowed for a non-income property.

Exam-friendly reminder: Interest may be deductible; principal is not. Depreciation is for income property improvements, not a typical primary residence.

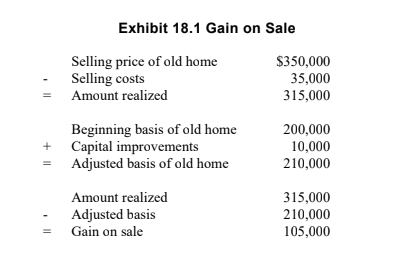

Tax Liability: Gain on Sale (How the IRS Defines “Gain”)

The IRS generally defines gain on the sale of a home as:

amount realized (net proceeds) minus the home’s adjusted basis.

Amount realized (net proceeds):

Sale price − Costs of sale = Amount realized

Sale price − Costs of sale = Amount realized

Adjusted basis starts with the beginning basis (often the purchase price plus certain settlement costs) and is then adjusted:

Adjusted basis:

Beginning basis + Capital improvements − Exclusions/credits/amounts received = Adjusted basis

Beginning basis + Capital improvements − Exclusions/credits/amounts received = Adjusted basis

Finally, the basic gain formula is:

Gain on sale:

Amount realized − Adjusted basis = Gain on sale

Amount realized − Adjusted basis = Gain on sale

Exhibit 18.1 — Gain on Sale

Plain English: Gain is basically “what you net from the sale” minus “what you have invested in the home (with adjustments).”

Gains Tax Exclusion (Primary Residence)

Tax law provides a gain exclusion of up to $250,000 for an individual taxpayer and $500,000 for married taxpayers filing jointly (as presented in the text),

generally available every two years if the taxpayer meets the ownership and use requirements.

- Owned the property for at least two years during the five years preceding the sale;

- Used the property as a principal residence for a total of two years during that five-year period;

- Waited two years since last using the exclusion for any sale.

Important: Losses are not deductible, and unused exclusion amounts do not carry over.

Quick Check-Ins (Self-Test)

1) The “amount realized” from the sale of a home is generally:

- A. Sale price plus costs of sale

- B. Sale price minus costs of sale

- C. Adjusted basis minus capital improvements

- D. Original price minus current value

Show Answer

Correct: B. Amount realized is net proceeds: sale price minus costs of sale.

2) Which item would typically increase a homeowner’s adjusted basis?

- A. Paying mortgage principal

- B. A capital improvement (like replacing a roof or adding central air)

- C. Paying property taxes

- D. Buying homeowners insurance

Show Answer

Correct: B. Capital improvements increase the adjusted basis of the home.